Banknote concerns are growing as the insolvency of small and medium-sized enterprises has intensified recently. As of May of this year, domestic banks' SME loan delinquency rate was 0.51%, up 0.05% from delivery. The Credit Guarantee Fund predicts the SME insolvency rate next year at 4.2%, which is higher than this year (3.9%). What banks need most is a “pioneering plan” that can separate superior companies from insolvent companies. However, more than 95% of domestic for-profit corporation operators are non-external audit firms without disclosure obligations. Financial information that can evaluate a company is limited. From a bank's point of view, a blind person has no choice but to evaluate companies as if they were touching an elephant.

I wonder if financial data is the only standard for evaluating companies. fintech startup Antockproposed an alternative credit evaluation model using non-financial data as a solution. Park Jae-joon, CEO of Antock, said, “We will provide banks with an opportunity to avoid insolvent companies, and new funding channels for companies.”

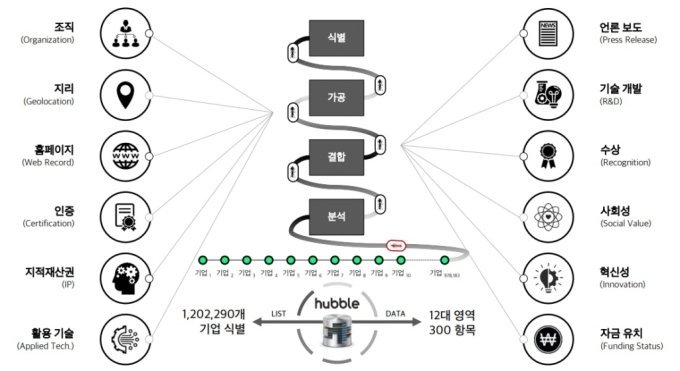

“We will catch corporate risks that are not in financial statements”

As the name suggests, Antock's alternative credit evaluation model “PULSE (pulse, pulse)” measures the pulse of a company. The biggest characteristic of Pulse is that it uses non-financial data. We collect and analyze more than 300 non-financial data, including server response, patent maintenance ratio, number of employees, and media reports based on △ freshness, △ frequency, and scale. CEO Park said, “It may not be shown in financial statements, but for example, the insolvency rate of companies that are not properly connected to the company's website is different,” and “the same goes for employment information. If the number of retirees has increased rapidly recently or media reports have declined significantly, it can be judged as a risk sign.” When companies were evaluated based on actual pulses, the bankruptcy rate of companies gradually increased according to the rating. It's different from the existing credit evaluation model where the default rate is concentrated on companies with lower credit ratings. Park Young-joon, director of Antock, who oversees the alternative credit evaluation business, explained, “When companies were evaluated based on actual pulses, the default rate of companies gradually increased slightly depending on the grade and showed a sharp increase from the lowest grade,” and “it is different from the existing credit evaluation model where the default rate is concentrated on a specific grade rather than the lowest grade.” Another role of pulse is to segment the credit ratings of companies focused on B to BB ratings. When evaluating domestic companies using the existing credit evaluation model, 86.8% of the total is concentrated on B to BB ratings.

Director Park said, “When using Pulse, the share of existing B to BB grade companies decreased by 54.5%. Instead, the BBB rating, which was only 8.8% in the existing credit evaluation model, increased to 21.3%, and the A grade, which was 2.1%, increased to 9.8%,” he said. “The existing credit evaluation model does not properly capture the characteristics of different industries.” For companies that have been tied to B to BB ratings, this is an opportunity to raise funds at low interest rates. In fact, in the case of e-commerce startup Company A, the predicted interest rate was 4.02% when evaluated by pulse, which was 3.28% points lower than the existing credit evaluation model (7.3%). Funding costs can be reduced by nearly half.

Finance Chairman's Award... Applied to card borrowers and Dongdaemun throughout the year

Pulse's performance has already been recognized in the financial sector. Last year, as a result of performing performance verification for small business loan owners through the IBK Corporate Bank Open Innovation Program “IBK First Lab (1st Lab)”, it received a “good” judgment. Since then, an alternative data delivery agreement was also signed for the development of an alternative credit evaluation model. In January of this year, it won the Grand Prize (Finance Chairman's Award) at the Finance Committee's 'D-Test Bed' based on a performance verification (PoC) case with IBK Corporate Bank. D-Testbed is a project that provides a test environment for fintech startups and prospective founders to verify the business performance of innovative technologies and ideas. In the second quarter of this year, performance verification was conducted for Lotte Card and corporate card owners, and it received an “excellent” rating. Antock and Lotte Card agreed to conduct a test commissioned by the Finance Committee to introduce an alternative credit evaluation model. The plan is to conduct an alternative credit evaluation for actual credit card owners throughout the year. KB Kookmin Bank is also developing an alternative credit evaluation model for small and medium-sized enterprises in the Dongdaemun fashion supply chain as part of the Korea Internet & Security Agency's fintech application program (API) development project. “It will play a role in improving the phenomenon of companies flocking to specific grades,” and “the goal is to start with a role that complements existing credit evaluation models and grow into an exclusive credit evaluation model in the future.” [Money Today Startup Media Platform 'Unicorn Factory']